ACH Processing: What It Is & How It Works

From accepting online donations to selling event tickets and branded merchandise through your website, the ability to facilitate digital payments effectively is absolutely essential for your nonprofit organization. Of course “effectively” facilitating payments means more than just ensuring donor details are processed correctly and valid transactions are going through.

An important factor for a positive payment experience is the ability to support major payment types, namely credit card processing, international transfers, and debit or ACH processing.

In this guide, we’ll break down the essentials of ACH payments and ACH payment processing so that you can make the most of this powerful payment type. We’ll cover:

- What Is an ACH Payment?

- How Does ACH Payment Processing Work?

- Benefits and Drawbacks of ACH Payments

- iATS Payments: The Best ACH Payment Processor for Nonprofits

While most nonprofits support simple credit card transactions, too many underutilize or entirely miss out on the capabilities of ACH payments. This convenient, secure, and versatile payment method can strengthen your fundraising efforts and open up the gates to a smoother, more accessible payment experience.

Let’s begin by exploring the basics of what ACH payments entail.

What Is an ACH Payment?

ACH payments are direct transfers from an individual’s bank account into a target bank account. For example, an individual donor might transfer funds from their bank account into a target bank account (ie: your organization's account) without the in-between step of a credit or debit card.

ACH payments, also known as direct debit payments, circumvent the need to process payments through a credit card network or other payment processing networks. Instead, they offer a direct bank-to-bank payment process through the Automated Clearing House.

What Does ACH Stand For?

ACH stands for “Automated Clearing House.” Run by the National Automated Clearing House Association (NACHA), this electronic payment network is used to “batch” and facilitate one-time and recurring donations, automatic payroll transfers, vendor payments, and other direct payments and deposits.

Types of ACH Payments

There are two main forms of ACH payment processing your organization should be aware of:

Direct Deposits

Direct deposits are payments made from a paying account into a pay recipient account, most of the time from a corporation or government entity to an individual. For your nonprofit, this might include your employee payroll system or the ongoing payments you make to your vendors or consultants. Alternatively, you receive direct deposits through benefits from the government.

Direct Payments

Direct payments are payment requests made to transfer funds out of a bank account. For example, this includes automatic utility payments your organization pays. Additionally, this also includes donations that are made to your nonprofit!

How Does ACH Payment Processing Work?

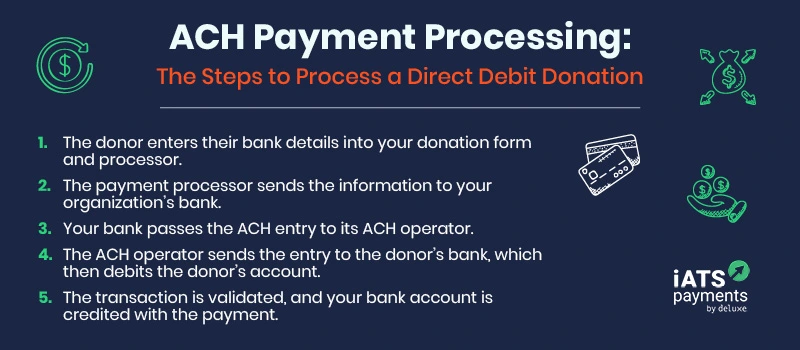

For anyone who’s still confused about the ACH payments and how the system operates, let’s take a moment to walk through what exactly happens during the ACH transfer and payment process.

Let’s use the example of a donor who submits an ACH direct debit donation to your nonprofit:

- The donor enters their bank details, namely their routing number, into your donation form.

- The data is captured by your payment processor, which sends this information to your nonprofit organization’s bank.

- Your bank passes the ACH request information to its ACH operator.

- Your bank’s ACH operator sends the information to the donor’s bank, which then debits the donor’s account.

- The transaction is officially evaluated and validated, and your bank account is credited with the payment amount.

Countless transactions of this kind occur every day through the Automated Clearing House, facilitated by donor generosity, banks, and—most relevantly for you—your chosen payment processor.

ACH Payment Processing: Key Terms to Know

ABA Routing Number

The American Banker’s Association (ABA) routing number is the 9-digit number on the bottom of checks. This number identifies which bank the check is from.

Authorization Code

An authorization code is the response code from the issuing bank returned to the nonprofit at the time of authorization.

Authorization Fee

This is also known as a transaction fee. It is the amount that is charged to a merchant account each time the payment processor communicates with the authorizing network.

Merchant Account

This is a type of enterprising bank account for businesses and other organizations that allows your nonprofit to facilitate, process, and accept different forms of electronic payments.

If you’re already accepting credit card donations, your merchant services provider may be able to help with direct debit donations as well. For example, iATS Payments by Deluxe offers both!

Benefits and Drawbacks of ACH Payments

ACH payment processing has both potential advantages and disadvantages for your organization. Consider these factors as you weigh the pros and cons of investing in an ACH-compatible payment processor:

ACH Benefits

Increasing Popularity

On average, the Automated Clearing House processes over 25 billion dollars in payments, deposits, and transfers, a significant amount of which includes the direct debit payments donors use to support nonprofit missions they care about.

And this amount is only expected to rise, with more people (like your supporters!) making use of this payment method. By offering ACH payment options to your donors, you can make the most of its increasing popularity.

Lower Transaction Fees

ACH direct debit payments only require a flat fee for each transaction. By contrast, credit card payments typically charge both a percentage fee and a flat fee for each transaction. This can mean spending hundreds or even thousands of additional dollars just to accept donors’ gifts.

Additionally, because donors change credit cards more often than banks, ACH payments allow your nonprofit to avoid bounced payments and more quickly process donations, online purchases, membership fees, and event tickets.

Recurring Donations

With ACH payment processing, donors can easily set up recurring donations that are directly debited from their bank accounts. Allowing donors to set up recurring donations automatically boosts your donor retention rates. As long as a donor doesn’t cancel the recurring debit, your nonprofit will retain that donor.

Security

Many people might be hesitant to share their bank account number online, but the process is actually quite secure. ACH payment processing uses encryption to essentially jumble the bank account numbers, keeping the info safe from hackers.

Additionally, your organization can fortify security even further by investing in PCI-compliant payment tools. This means that the software has passed the most rigorous security standards set forth by credit card companies.

Accessibility to Donors Without Credit Cards

Not every single donor has a credit card. While some of these donors can simply donate via check, offering them an ACH payment processing option allows them to give easily online.

ACH Drawbacks

Donor Hesitancy

Even though many donors will give out their credit card numbers online to make purchases and donations, many are wary about using their bank account number to give online.

What donors don’t know is that ACH payment processing is just as secure if not more secure than credit card payment processing. This is because the Automated Clearing House is a heavily regulated and controlled system and, should any fraud take place, users are protected under federal law.

Intimidating Process

Most people are familiar with entering their credit card numbers on an online form. However, few know their bank account numbers off the top of their heads, and even fewer remember their bank’s routing number.

To address this, you can ease donors into the process of using ACH direct debit by showing them where to easily find this information. Include an image of a sample check on your donation form that shows donors where their bank account and routing numbers are. Alternatively, most mobile banking apps will list users’ routing numbers when they’ve securely logged on.

Lack of Real-Time Transparency

It can take anywhere between 3 and 45 days to return or decline an ACH transaction if the donor inputs the incorrect information or if there are insufficient funds in the account. This creates a lag in transparency for nonprofits.

Unfortunately, there isn’t really a solution for this particular problem. It’s best for nonprofits to treat all ACH donations as “pending” until the funds are deposited into the account.

iATS Payments: The Best ACH Payment Processor for Nonprofits

From its security and simplicity to its wider accessibility than typical credit card payments, ACH payment processing is a powerful tool that can empower your nonprofit to create a more positive payment experience and increase its incoming revenue. However, in order to facilitate ACH payments in the first place, you’ll need a robust payment processing system that supports ACH transactions.

This is where iATS Payments by Deluxe can be a boon for your nonprofit organization. iATS Payments is one of the most trusted and intuitive payment processors in the nonprofit sector, supporting not only ACH payments, but credit processing and even international payment processing.

ACH Processing & Other Top Features

With the iATS payment processor, nonprofits can streamline ACH and credit card payments together and individually within a single merchant account. Our team works with you to create the ideal payment processing solution that suits your organization’s needs and your supporters’ preferences.

As donations, event tickets, and other payments are processed, the iATS portal offers up-to-date details on in-progress and completed payments, as well as any discrepancies that may crop up.

Efficiency, accuracy, and security are the guiding principles used to design our fully integrated, Salesforce-native payment processor. In addition to the various payment methods we can streamline for your organization, the iATS payment processor also boasts:

- Level 1 PCI security compliance

- Tokenization, encryption, and other anti-fraud tools

- Complete integration capabilities

With our comprehensive payment processing solution, your organization will be equipped with all of the features you need to create a safe, secure, and streamlined donation experience.

Additional Resources

- Nonprofit Payment Processing: Buyer’s Guide. Explore our dedicated payment processing manual and buyer’s guide to begin your search for the best ACH-compatible payment processor.

- Accepting Donations Online: The Ultimate Guide (& 11+ Tools). Learn more about accepting, optimizing, and finding tools to facilitate electronic payments with our definitive guide to online donations.

- Why Credit Card Processing Matters for Your Business. ACH processing isn’t the only form of payment processing your organization needs to support. Read up on credit card processing to round out your knowledge.